Agency Theory, Game Theory, and Procurement Cost Avoidance

The role of cost avoidance in procurement savings management

Cost-saving has always been an essential and high-visibility priority for the procurement function.

Despite the declared accountability for efficiency and effectiveness, the cost-saving goals remain the primary procurement performance measure.

Meanwhile, cost avoidance remains largely an internal KPI known to executive stakeholders but needs to be measured and reported consistently.

This post will examine some essential prerequisites of cost avoidance recognition and apply the renowned economic theory to the procurement process.

Agency Theory

Agency theory (or principal-agent model) is one of the building blocks of the Theory of the Firm.

An agency relationship is created when a person (the principal) authorizes another person (the agent) to act on their behalf.

Then, the firm is viewed as a set of contracts between self-interested actors seeking to maximize their personal (economic) gain.

Principal vs. Agent problems

Central problems in agency theory are:- the conflict in goals between the principal and agent,

- information asymmetry, i.e., agents have more information than the principals, which also has two instances of

- adverse selection or pre-contractual opportunism (buyer's lack of accurate information about the object of sale)

- the moral hazard of post-contractual opportunism (attempt to defeat contractual goals to seek self-interest.)

How to overcome moral hazard (Game Theory)

The consultant has more technical expertise (information asymmetry) and can:

- Choose the best supplier for the company (Supplier A) and help the company generate extra revenue of £200,000.

- Choose a suboptimal supplier (Supplier B), resulting in a £50,000 loss for the company, in return for a Supplier B commission (£40,000.)

The challenge is to use game theory to align the consultant's interests with the company’s goals, i.e., to find the Nash Equilibrium.

Nash Equilibrium

Nash Equilibrium is a central concept in Game Theory. It is used to analyze strategic interactions between players (decision-makers) where each player’s outcome depends not only on their own decisions but also on the decisions of others.

It represents a situation where no player can improve their payoff by unilaterally changing their strategy, given the strategies chosen by the other players.)

The company can offer a performance-based contract (e.g., 25% of extra revenue) to incentivize the consultant to choose the best supplier.

In this case, the Nash Equilibrium occurs when the consultant selects Supplier A and receives a higher total payoff (£70,000).

In this case, the Nash Equilibrium occurs when the consultant selects Supplier A and receives a higher total payoff (£70,000).

Payout table

Supplier A (Best Choice) | Supplier B (Commission) | |

Basic Contract | Consultant: £20,000 Company: £200,000 | Consultant: £60,000 Company: -£50,000 |

Performance-Based Contract | Consultant: £70,000 Company: £200,000 | Consultant: £60,000 Company: -£50,000 |

Cost reduction vs. cost avoidance or hard vs. soft savings

Cost reduction means the positive difference between the earlier item's price and an actual one.

Sometimes, it is referred to as "hard saving" due to its direct and measurable impact on the company's bottom line results. It is easily traceable and verifiable.

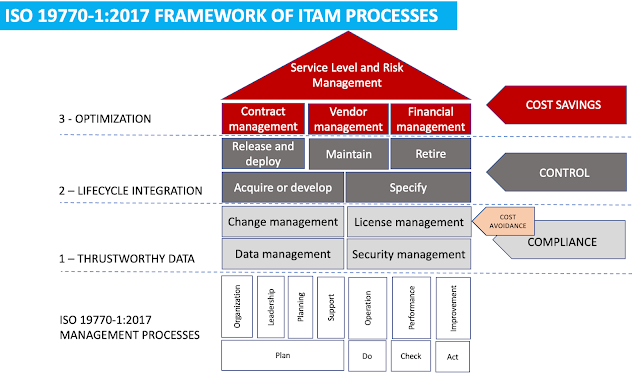

Cost avoidance or "soft saving" means preventing various procurement costs. This broad category includes:

- fully or partially avoided price increase and/or indirect expenses (logistics, repair, maintenance, consumables, etc.)

- provision of goods or services over and above the required scope of supply,

- improved payment terms,

- budgetary savings vs. pre-sourcing projections.

The ambiguity of recognition and reporting cost avoidance leads many companies to omit this performance indicator.

Applied Agency Theory in the context of procurement savings management

The following research provides clear and practical conclusions on procurement savings management based on the postulates of the Agency Theory that were explained earlier.

Principals tend to recognize cost avoidance, given the limited opportunity for cost reduction.

Once the cost reduction potential is depleted, principals start looking favorably at other performance indicators.

Due to the information asymmetry between the principal and the agent, reporting and monitoring must be established to maintain the principal's perceived control.

Therefore, any relevant metric is better than the absence thereof. With all due respect to cost avoidance, it's just an instrument for executive oversight.

Goal incongruence, information asymmetry, self-interest, and bounded rationality affect the principal's position on cost avoidance.

Objective and subjective factors affect the position of the principle as such.

Their position on cost avoidance is a subset of executives' boundedly rational, ill-informed, politically influenced, and opportunistic behavior.

Principals' perception of cost avoidance affects purchasing agent behavior

This point nicely formulates the human side of the cost avoidance topic.

Procurement personnel will exercise passive opportunism and not pursue avoidance if the principal doesn't care.

Cost avoidance requires resources to manage its tracking and reporting

Quality reporting cannot happen by putting an extra load on overworked agents.

It must be clearly defined in governance terms, supported by appropriate tools, and adequately staffed by trained and motivated executors.

The problem of cost avoidance

Multiple issues with cost avoidance may be generalized to other conflicts in procurement (and not only it.)

Excellent cost avoidance opportunities may be overlooked because the procurement agent is not motivated, rewarded, or equipped to pursue and achieve those goals.

A rational person is unlikely to work hard to achieve an avoidance and then have it dismissed as lacking credibility. Such a person is likely to exercise passive opportunism instead.

The principals' role will be to control and monitor an agent, negotiate the importance of cost avoidance with peers, and establish processes, means, and resources to provide quality analysis.

The starting point is the procurement principal's confidence in the importance of cost avoidance for the firm's performance. Surprisingly, this still needs to be corrected for some colleagues.

P.S. If you appreciate hundreds of hours invested in researching and writing this blog, you can buy me a coffee or subscribe for the membership by following this link. Thank you!

More information on this and other exciting topics can be found in "The Technology Procurement Handbook." It represents 23 years of experience, billions of dollars worth of successful sourcing projects, and 1000s hours spent on research, analysis, and content creation for the most demanding professional readers.  |

Comments

Post a Comment